Beyond transactions: Why the future of global commerce depends on a smarter payment strategy

Why modern merchants need multiple payment vendors

Expanding into new markets should be a growth driver, not a logistical nightmare. Yet, when it comes to payments, most global merchants face five core challenges — and often, all at once:

- Regulatory and compliance hurdles: Every region comes with its own set of financial regulations. Think PSD2 in Europe, RBI guidelines in India, PCI DSS and local anti-money laundering laws. Non-compliance doesn't just lead to failed transactions — it can result in legal risk and brand damage. Staying compliant often requires local partnerships.

- Currency conversion and FX costs: Selling internationally means navigating volatile exchange rates and hidden conversion fees. A few percentage points here and there can quietly erode margins, especially at scale. Plus, customers don’t like paying in unfamiliar currencies; they expect localized pricing and settlement.

- Payment method fragmentation: Did you know that Alipay accounts for over half of China's online payments, or that iDEAL is the default in the Netherlands? Global customers don’t just prefer local payment methods — they often won’t complete a purchase without them.

- Transaction failures and fraud: Cross-border transactions get flagged more often. Fraud detection systems, while necessary, can inadvertently block legitimate payments, especially when banks don’t recognize your processor. This leads to false declines and lost customers.

- Settlement delays and high processing fees: Legacy payment rails can take days to settle funds, creating cash flow bottlenecks. Processing fees vary widely across countries and providers, adding financial unpredictability.

Why payments must be reimagined — now

In a world of instant gratification and borderless commerce, payment should be the last thing slowing you down.

Let’s explore the key reasons why merchants are moving beyond traditional payment systems and toward flexible, modular architectures.

Localization is a conversion driver

Customers feel more comfortable paying in their local currency and using their preferred method. A Baymard Institute study found that 9% of shoppers abandon their carts because there aren’t enough payment methods available.

You fill your cart, hit checkout… and your go-to payment method isn’t there. So you do what any shopper would: Abandon the cart and pretend it never happened. Retail therapy: Canceled. That’s exactly how digital shoppers feel when they don’t see familiar options like PayPay, PIX or Klarna.

Localization isn’t a perk: It’s a prerequisite for trust.

UX matters more than ever

Trust is fragile online. Payment flows must feel seamless, intuitive and secure. Features like one-click payments, biometric authentication and wallet integrations (Apple Pay, Google Pay) have become industry standards.

A clunky, multi-step checkout with an unfamiliar processor? That’s how you lose a sale in 3 seconds.

Flexibility future-proofs commerce

Markets evolve. Regulations change. New payment tech (like BNPL, crypto and real-time rails) emerges every year. If your stack is rigid, you’re always playing defense.

Composable architectures let you plug in what’s needed without breaking your existing setup.

How commercetools Checkout puts merchants in control

At commercetools, we’ve seen this pain firsthand. That’s why we built the commercetools Checkout, a fully composable, vendor-agnostic solution that lets merchants design and manage checkout and payments like never before.

Plug-and-play integration with best-of-breed vendors

Choose from world-class processors like Adyen, Stripe, Klarna or local specialists. Need to add a provider in a new region? Do it instantly and without a single line of code.

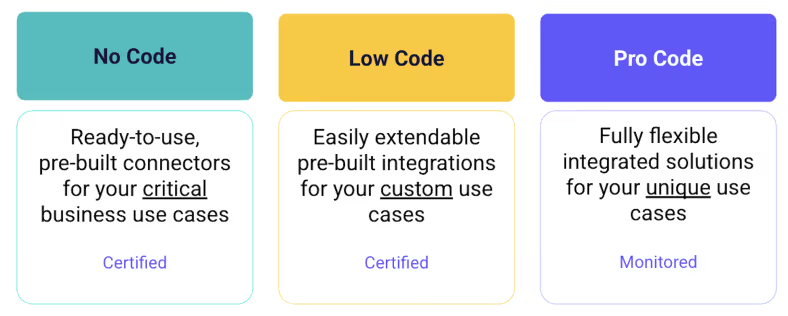

No-code, low-code and pro-code support

From business users to developers, everyone has the power to configure, test and deploy payment flows at their own pace. Want to prototype a new BNPL method for Europe? Use no-code connectors. Launching a custom checkout experience? Use low-code templates. Need total control? Go pro-code.

In short: One platform, endless flexibility.

Real-time customization and experimentation

commercetools Checkout lets you swap providers on the fly, A/B test experiences and create conditional logic based on geographies, currencies or customer segments.

For example:

- Route US traffic through Stripe.

- Use Klarna for EU customers under 35.

- Show bank transfer options only for high-value B2B purchases.

All are configurable without waiting for quarterly dev cycles.

Composable, modular, scalable

As with everything at commercetools, our composability-first mantra applies. commercetools Checkout fits into your commerce architecture as a service — not a monolith. Build what you want. Scale how you need. Stay future-ready.

Why it matters: Modern payments are business-critical

Modern commerce is global, fast and customer-first. But legacy payment systems were built for another era — one where slow, expensive and inflexible were the norm.

With commercetools Checkout, you’re not just adding more providers. You’re gaining:

- The freedom to scale without friction.

- The tools to build trust with local customers.

- The agility to adapt to change — on your terms.

Payments shouldn’t be a hurdle, but an advantage. commercetools helps make that possible.

Learn more about commercetools Checkout.

Senior Product Manager specializing in checkout and payments. She leads initiatives to create seamless and reliable commerce experiences, improving journeys for both merchants and consumers. Passionate about innovation and user-centered design, Esra strives to make commerce more efficient, intuitive, and accessible for everyone.

.svg)